A key feature of most highly successful businesses is a strong economic moat. Moats are means/methods of maintaining competitive advantages over competitors and potential new entrants in a market. The concept, symbolizing the same as a moat around a castle, is meant to evoke protection and strength.

(Seeking Alpha)

Strong moats lock a company and their offerings into regular customer use. They are aided by stickiness of a product, which is essentially the degree to which it becomes difficult to stop using said product. This is extremely valuable when you can extract all of the value out of that product thanks to customers using it regularly.

One company whose moat has been strong and continues to grow is Square. You’ve almost certainly come across them in a restaurant or small business, maybe you have the Cash App. Either way, they’re close to a household name at this point, and their CEO, Jack Dorsey, is a big name executive to boot (he’s also the CEO of Twitter). Square is an enormous fintech company with products spanning financial services, digital payments, and hardware.

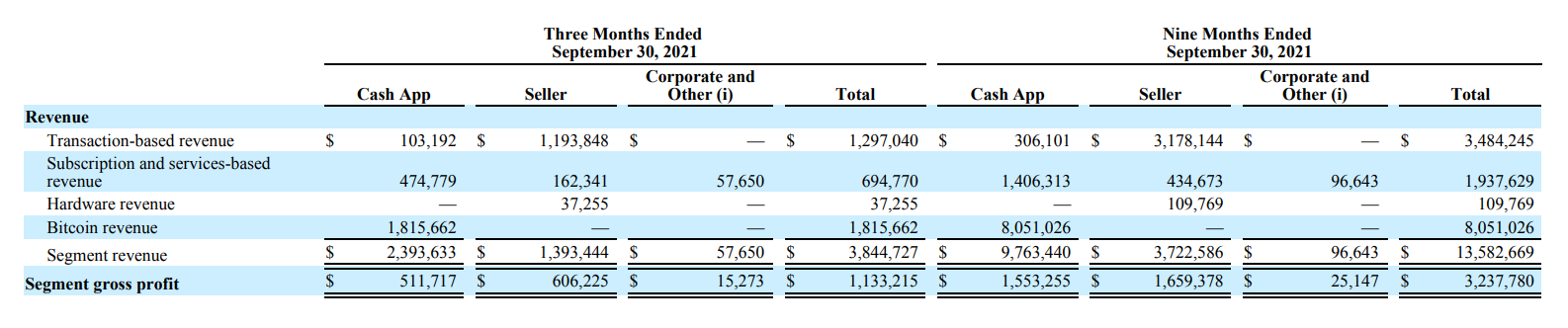

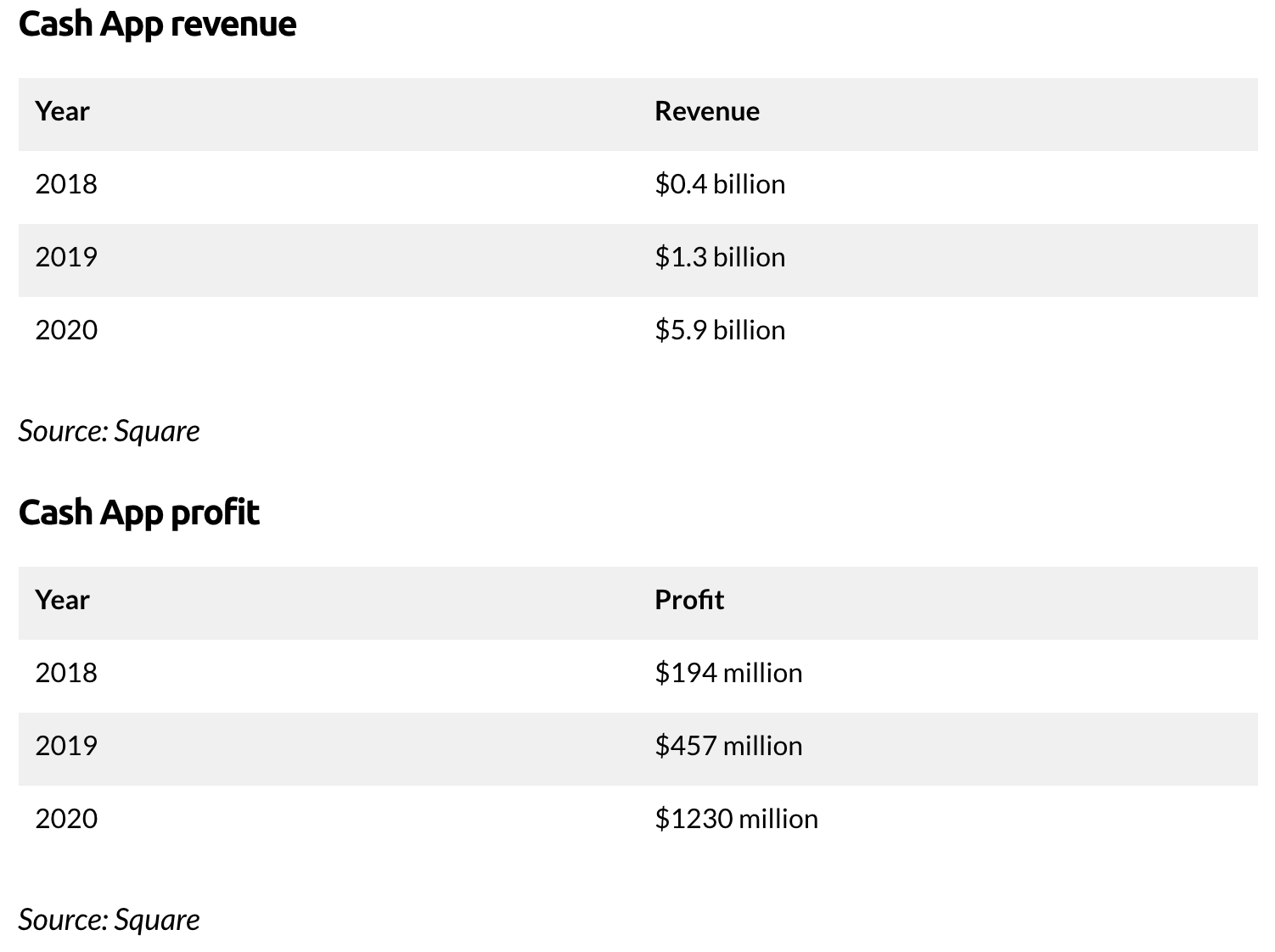

Cash App is one of Square’s most successful products because it’s consumer-focused. It’s a competitor to Venmo and PayPal, but offers a suite of features that the others do not (as you can see in the table above, that’s paid off!). It comes with a bank account, debit card, investment capabilities, and more. A full financial suite at your fingertips is a powerful tool and that’s proven to be evident with Cash App’s incredible growth. The product has grown at a 50% or greater clip since 2016 and as of last year had 36 million monthly active users and 70 million annual transactors. Most of the Cash App userbase tends to skew younger and underbanked. Network effects propelled it ahead of Venmo in popularity recently and its focus has snapped into place with its demographics.

Recently, Square announced a new feature for their product suite - Cash App Pay. It enables Cash App users to pay for items in stores directly or online with their Cash App balances and sellers to accept payments via their Square products. All transactions are contactless via QR code or button tap, which leads to a seamless and intuitive process for both payers and sellers. It enables omni-channel and contained payment flow entirely within the Square ecosystem, which is by definition an incredibly strong moat.

As I wrote about Visa in The Other Sleeping Giant of Payments:

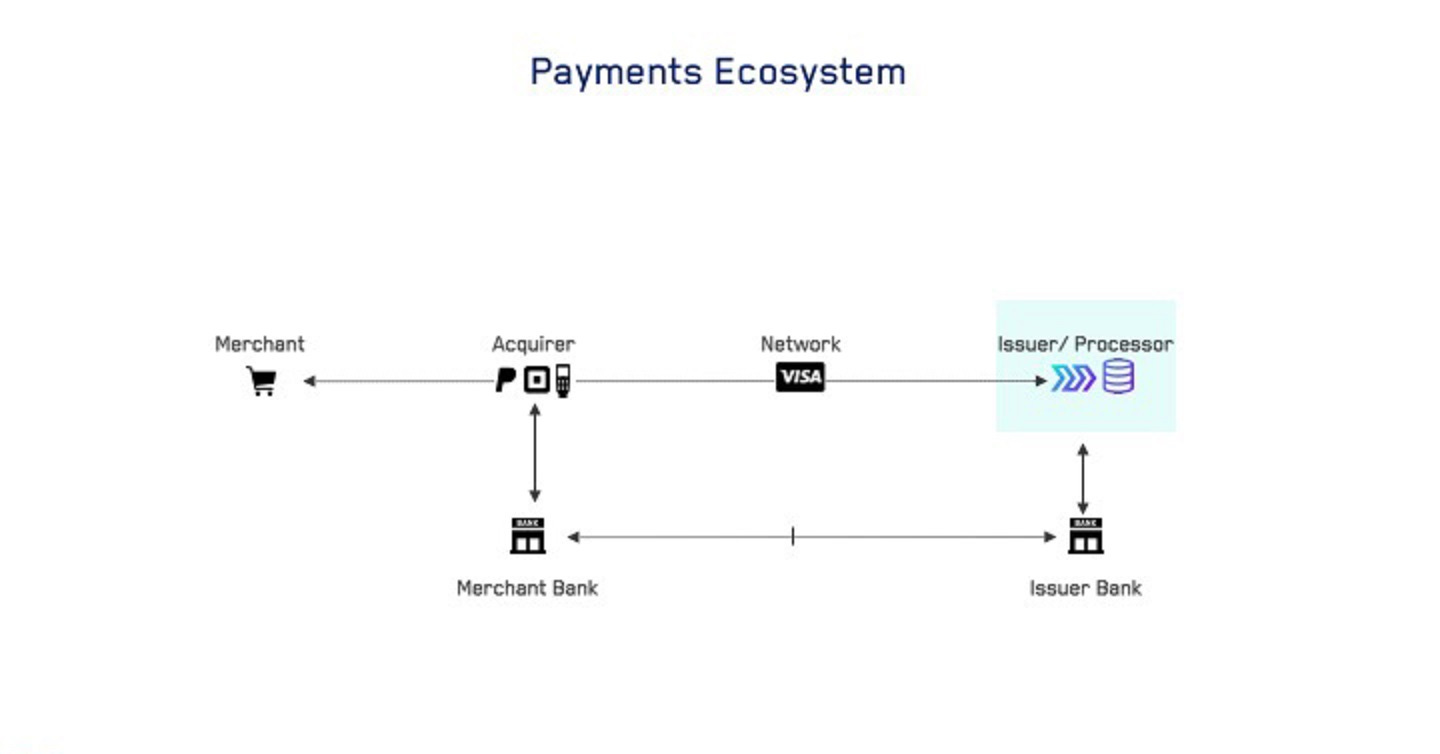

When payments are made, information has to flow to several places quickly. The store has to acquire your funds, those funds need to be both confirmed in your bank account or credit line, those funds need to be processed and debited from your account, and then returned to the store through their unique ID. That data flow is powered through networks known as payment rails that confirm accuracy of funds and information.

The ownership of a payments ecosystem and payment rails propelled Visa to processing more than 150 billion transactions a year and $9 trillion in GMV. Visa and MasterCard have net income margins close to 50% and EBITDA margins that can reach 70%. This means that each business is very profitable and has high cash flow. Square enabling payments within its own ecosystem means it doesn’t lose value to the incumbent payment rail companies, but can essentially create its own rails. Maintaining and owning it’s own system means money never leaves Square’s infrastructure. As the saying goes, “your margin is my opportunity”.

Jareau Wade wrote about this for Fintech Today recently and explained the process well. When you pay for something on a Square machine at a store, say a $4 coffee, Square takes ~3% of the value of the transaction as their “take rate”. 2/3 of that ~3%, or $0.08, goes to the network and issuer bank (e.g. Visa and JP Morgan Chase). But if Square can handle all of the above, it would stand to keep all of that transaction take rate. It’s a literal closed-loop economy within the payment giant’s infrastructure and suite of products. Without revenue leakage.

Adding buyer and seller payments/acceptance adds to the stickiness of the Cash App and store products because of the simplicity of doing all of your business in one place. Having money in Cash App makes your life easier. Especially when you can invest it, get it from an atm, or something else. That’s very different than Venmo, where many people try to cash out as soon as possible.

So if you combine a viral and rapidly growing Cash App customer base with a closed payments ecosystem, you have the makings of a disruptor for the big four payment rails companies (Visa, MasterCard, Amex, Discover). Their stranglehold has captured all of the returns for decades, but as the world shifts entirely digital, can Square take that lead. So what else needs to go right for Square to keep their momentum high?

The simple bullish case is that Square continues to rollout products and acquire customers who want to stay in their ecosystem. More customers means more dollar flow through its many pipes and products and less of a desire for churn. The incumbents also can’t reduce their take rate without destroying their margins and revenue. Now for the bears. Visa et al are very well aware of this and have invested heavily in digital infrastructure and even crypto to keep pace. Similarly, these incumbents are heavily entrenched in areas/companies/stores that don’t quite have see the switching allure.