The Other Sleeping Giant of Payments

Everyone is obsessed with Stripe, and rightfully so. But Stripe can't exist on its own.

The last few weeks have been absolute love zests of Stripe, and rightfully so. Stripe is an incredible company who no doubt will go on to revolutionize finch even further. If any sort of process or technology touches money over the next 10 years, I imagine Stripe will be involved 60% of the time or more. Stripe, per Stripe, “ is a technology company that builds economic infrastructure for the internet. Businesses of every size—from new startups to public companies—use our software to accept payments and manage their businesses online.”

Stripe has been covered by every journalist, blogger (favorite 1 | and 2), and podcast. All are must reads because Stripe might be the best run and most impressive company out there that most people haven’t heard of. On the other hand, Visa, a company you’ve heard of if you’ve left your rock in the last 60+ years, is sneakily one of the most impressive companies in the fintech space.

Visa has already partnered with Stripe, and it looks as though they understand the role each will play moving forward with a symbiotic relationship. Most recently, Visa worked with Stripe to create a digital payments card that enables buyers to pay suppliers who previously were not plugged into a digital banking infrastructure. Suppliers are able to register through one of Stripe’s products, Connect, enter some banking information, and will quickly and efficiently enable suppliers to accept payments. Chavi Jafa, head of Business Solutions in Asia Pacific said:

“Migrating to digital payments benefits both buyers and suppliers, as it eliminates manual processing and enhances reconciliation. This improves productivity while reducing errors and fraud. It also allows buyers and suppliers to better manage their working capital, utilizing a Visa Commercial Card”

But Stripe isn’t the only digital payments company that Visa has recently partnered with. A startup, BlockFi, recently partnered with Visa to release a credit card offering Bitcoin rewards instead of the normal alternatives. It is close to inevitable that Bitcoin will be “a thing”, as it’s an asset that implicitly has value. Visa has been involved in what is a long term play that comes with little downside. It also partnered with Coinbase for a debit card.

On the other side of the fintech universe, Visa has been in attempts to buy Plaid. If you haven’t heard of Plaid, that’s part of the point. But if you’ve ever linked your bank account, Robinhood, credit card, etc. to an app it was likely done with the help of Plaids API connecting your account to the app you’re using.

What Visa excels at is enabling other “companies new to the payments universe [to] piggyback on Visa’s established technology and connections when building out their own capabilities, giving the newcomers a head start on some of the more behind-the-scenes aspects of payments and giving Visa a role in emerging ways of paying.” Visa provides all of the digital payments infrastructure necessary to carry out a payments, the fintech companies just need to add their own technology to the respective stacks. Visa has put itself in a position to touch most of the money being passed round the globe, establishing its own spiderweb of payment frameworks. While Visa doesn’t necessarily care if a payment ends in a Visa account, as long as part of the transaction passes through their web, then it’s a win.

Visa’s Fast Track program, described above, its a self-fulfilling pipeline to visionary startups. Partnering with some notable startups already (e.g. Chime and Rappi), Visa provides all of the go-to-market tools a fintech startup might need to succeed. But what makes Fast Track even more powerful than just providing advisory services, payment frameworks, and APIs is that is connects these other fintech startups with established partners like Stripe or Marqueta. Fast Track has seen a 360% increase in the program over the last year.

Separately, Visa has worked hard on international expansion - partnering with companies like Alibaba for equipping travelers with Alipay. Visa also has a lead in Europe over competitors like MasterCard, but that lead is slowly dwindling.

Visa is very transparent about its lofty goals for payment innovation. Everything from cars, to home appliances, to literal retail stores can be updated - in their mind. Visa has the scalability to make all of their ambitions come to fruition, in an ever growing market. The reason that Visa is so scalable is because of the network effects its privy to thanks to being a payment rails manager.

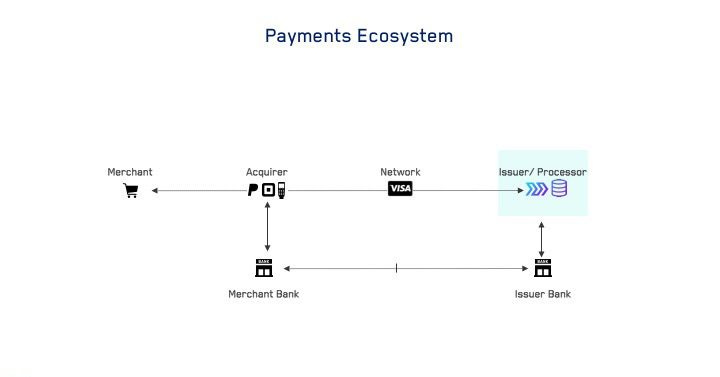

When payments are made, information has to flow to several places quickly. The store has to acquire your funds, those funds need to be both confirmed in your bank account or credit line, those funds need to be processed and debited from your account, and then returned to the store through their unique ID. That data flow is powered through networks known as payment rails that confirm accuracy of funds and information. Visa is the largest of these card rails (also includes AmEx, Mastercard, etc.). For context, Visa processed 140.8B transactions in 2019, and over $8.8T (!!!) in payments according to their 2019 annual report.

2020 was a disastrous year for multiple reasons. We are currently in a recession and have seen a historical drop in consumer spending (which has recovered) that looks like it may repeat in some ways as we approach a potential second wave of lockdowns. Despite all of this, Visa still almost matched its FY2019 figures. Because digital payments are thriving, and look to continue to do so.

What’s maybe most impressive, though, is that Visa’s network of payment rails is strong and cheap. Network and processing costs, according to the most recent 10-K amounted to $727 million - compared to data processing revenues of $10.98 billion, a rouge margin of around 93.4%. . There likely are some other costs (e.g. in the D&A and professional fees) that would reduce margins a bit more but aren’t specific in the letter. But on surface level, not only are those margins incredible, but they’ve been improving year over year. 2018 saw a margin of 92.4% and 2019 saw one of 93.1%

Visa is set up for continued network and transaction growth with minimizing costs. As it looks to grow internationally and continue developing its partnerships with current (and future) fintech darlings. The core tradeoff with Visa emphasizing its capabilities to support newcomers and having a high-margin network, is that they have suffered market share to MasterCard and others across Europe and elsewhere. S&P quoted another tradeoff below:

Visa is targeting acquisitions of or partnerships with the networks, while Mastercard is focused on owning the assets to operate the networks itself.

There’s tons of space for growth for the two card providers, but my money is on Visa.