Feature Fragmentation

Feature Fragmentation

As big banks lose market share to fintechs, their "features" become behemoths

I’m back! Took a hiatus in July for the 4th, a vacation, and going through the horrible process of moving in New York City during the summer. But now that I’m settled we can get back to our regularly scheduled programming.

On Sunday, fintech giant Square announced that they were going to purchase another fintech giant, Afterpay for $29 billion dollars in stock. It’s one of the largest fintech acquisition prices ever, and the largest for an Australian company. For those unfamiliar, Afterpay is a “buy now, pay later” (BNPL) provider, similar to an Affirm or Klarna. It’s one of the companies that hangs by the checkout when you shop online and offers the “or, pay $X for Y months with Afterpay.”

(Source: Square acquisition overview)

Afterpay is a savvy purchase for Square for a handful of reasons. First, it has over 100,000 global merchants using its platform and over 16 million customers, which can help enhance Square’s growth and footing with sellers. Second, it extends Square’s breadth of offerings and can be easily combined with its existing products, like Cash App. Third, Square missed the mark of building this in house, and making up that ground would have been a steep endeavor. Per Jack Dorsey, Square’s CEO:

Square and Afterpay have a shared purpose. We built our business to make the financial system more fair, accessible, and inclusive, and Afterpay has built a trusted brand aligned with those principles. Together, we can better connect our Cash App and Seller ecosystems to deliver even more compelling products and services for merchants and consumers, putting the power back in their hands.

Last year, BNPL services processed over $20 billion in transactions in the US alone and its users tend to skew heavily towards Gen Z and Millennials. Its also recently shifted from solely supporting the large-purchase infrastructure (Peloton’s, TV’s, etc.) to smaller items as well, like clothing. While the allure of points will hold steady for a bit, there has been a noticeable shift away from purchasing with credit cards and receiving lending from banks thanks to BNPL companies. Paying a fraction of the total cost of something monthly is a fraction of the burden of exceeding your credit card limit with one purchase in a month.

Jamie Dimon, CEO of JP Morgan, in this year’s investor letter said that “banks are playing an increasingly smaller role in the financial system”. All of the pieces of that system, which used to be run by banks, are being broken out into different fragments and handled by some fintech player in the industry. This is why “industries” like BNPL, retail trading, and retirement planning are not just features, they are actually enormous players fragmenting an incumbent system. They were features of the enormous banking system for years, but banks have become antiquated and inaccessible.

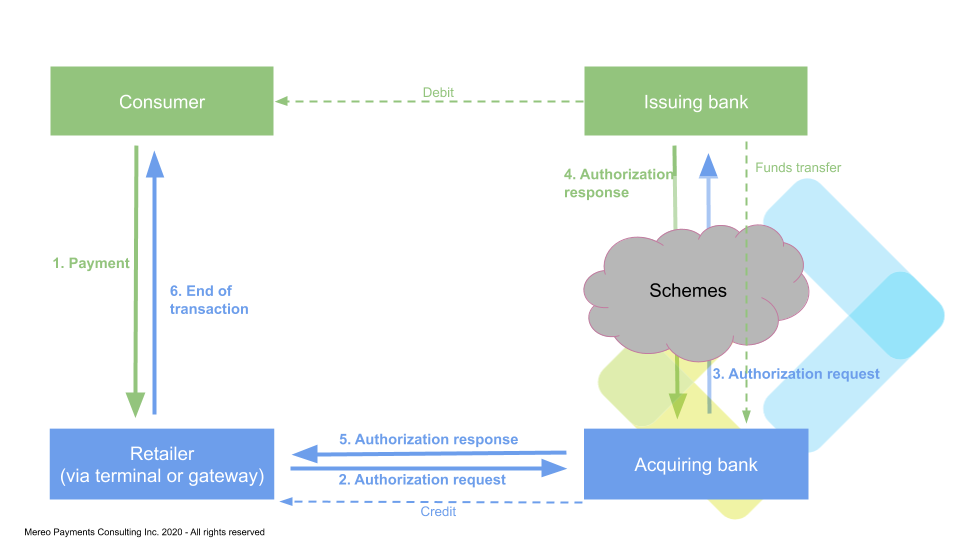

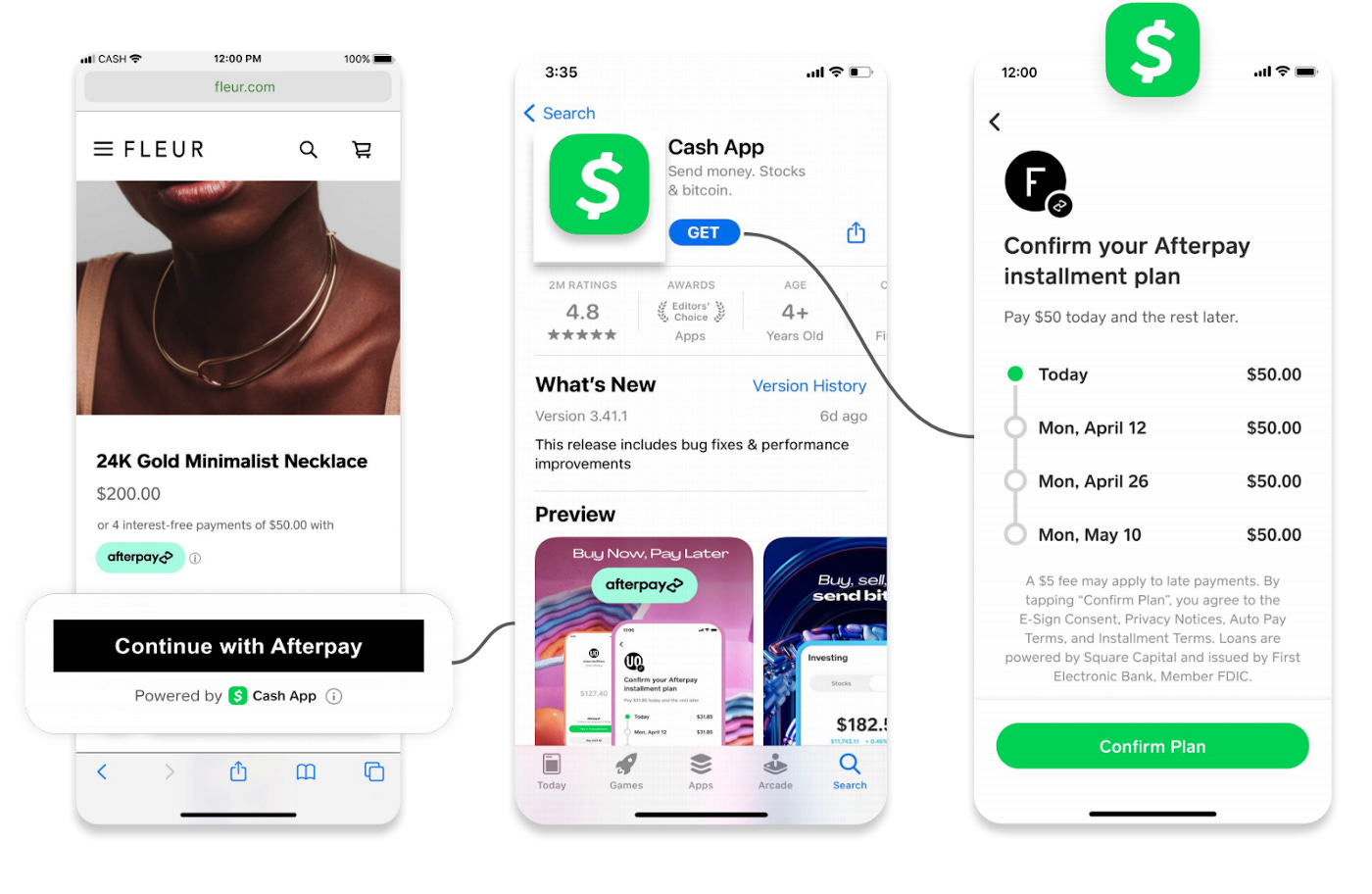

Someone in the Fintech Today Slack mentioned something pretty fascinating about what Square now can do. Square now directly “serves or owns three of the parties in the four-party payments system”. Square owns the technology that a retailer will use to process and accept the payment a consumer will make. Square then will send that transaction to the acquiring bank, in this case Afterpay, which requests approval from the issuing bank (Cash App). Since the issuing bank is also Square, and if there are funds in the Cash App account to pay for the purchase, Square will send the approval response back to the acquiring bank (Afterpay), and Afterpay will then process the transaction. What’s missing in Square’s arsenal is the payment rails, which I wrote about when deep-diving into Visa. Until then, they will own 3/4 of the transaction system.

Jack Dorsey is a noted bitcoin stan. *The blockchain enters the chat*.

Afterpay clearly becomes the lender in this case and not just a feature, but a company worth its own fraction of the four-party system. While they may now be considered an extension of Square’s reach, they are actually becoming an integrated partner in Squares broader fintech ecosystem that makes the full payment network ambition possible. It also shows that a growing trend towards the future of payments and banking will revolve around the consumer.

Companies like Afterpay will likely continue to be acquired over the next few months/years as the fintech market consolidates, with all larger players wanting to bolster their consumer credit arms. Rumors have emerged about Shopify buying Affirm, and Apple just recently struck up a deal with Affirm for BNPL purchases in Canada through Apple Pay. More and more consumer-focused fintechs will likely become household names.

(Source: Commerce VC)

We’ll see more acquisitions of some other BNPL companies soon, but also other “feature” type companies which have taken market share from the big banks as a larger wave of fragmentation. Fintechs are popping up and taking each limb off of the incumbent offerings and that disruption will continue. Its a democratization of products that were previously only available to institutions and high net worth individuals. In a decade our financial and payment system landscapes will look completely different as they’ll likely start to consolidate again. Square is poised to dominate a huge portion of that, and others like Stripe and Plaid will also entrench themselves.