Barely Charged

Barely Charged

A look at electric vehicle batteries and where their market may be headed

Last week the ARK Big Ideas 2022 report was released and it’s a treasure trove of information. Some of it is already known, some is new, but each section has valuable data that helps readers form opinions on the impact of technology over the next decade. One of the sections that stood out to me was a spotlight on Electric Vehicles (EV). Everyone knows Tesla, but most missed and eventually were priced out or avoided the volatility on the stock. But the ARK report actually mentions Tesla about as frequently in the Bitcoin section as they do in EV. It’s a more interesting, macro view.

What’s most interesting to me is the view into EV battery composition and the potential growth of the industry. Before we jump into why, let’s talk about how EV batteries work. In all batteries, when charged, electricity flows from a negative electrode (anode) to a positive electrode (cathode). This is powered by an electrolyte material (not Gatorade). Currently, most EVs use lithium batteries, which just means that the flow occurs because of positively charged lithium ions and a lithium metal oxide cathode. The anode is typically made of graphite or silicon and the electrolyte is actually liquid. But according to the University of Houston Energy Fellows, one of the biggest challenges with litium-ion batteries is that not a lot of energy can actually be stored.

… In concrete terms, this has limited how far EV cars can drive before they need to be recharged.

The obvious solution is to increase the energy density of the battery. An immediate option for doing so is to make the anode itself from lithium. It’s attractive because of lithium’s energy density and low weight, both of which would give EVs additional range.

All that said, working with lithium as an anode is particularly difficult for several very technical reasons that I won’t dig into here. EV builders are in a tricky position, though, because lithium is the most viable future material as cobalt, a current “competitor” is rife with humanitarian issues. Nickel is another material that’s critically important because it often pairs with lithium. Elon Musk once said “It’s also worth mentioning that although something is called lithium-ion, the actual percentage of lithium in a lithium-ion cell is approximately two percent. So, I mean, technically our cell should be called a nickel [battery]”.

(ARK)

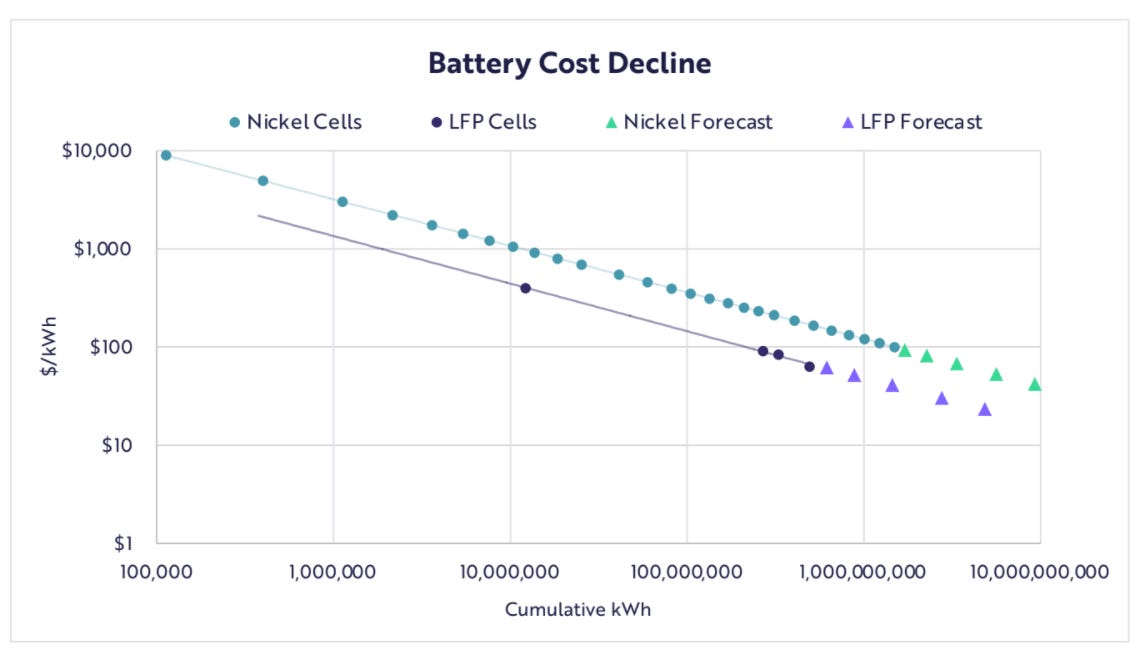

Aside from the scientific difficulties that are beyond my understanding, the additional tricky part with EVs lies in the economics of mining the material. The exploration and developments for mining lithium have improved, but the downstream supply chain and production issues that will follow aren’t braced for the exponential growth coming beyond the next three years. As you can see in the chart below on the left, most growth occurs in what’s called the S curve (in green), where a technology grows incredibly quickly then starts to plateau just as quickly. EV sales have actually looked more like a exponential growth…

The big issue with that expected growth is that ~67% of downstream lithium-ion battery production is in China, which comes with an enormous mixed bag of implications. Unless the US and most of the rest of the world wants to continue to depend on China for another critically important technology, some changes will need to be made. Vertical integration by EV companies or new manufacturing and production is possible, but a huge undertaking. Tesla, for one, could very easily swing its huge swaths of free-cash-flow ($2.8B!!) to mine lithium and essentially start a whole new subdivision of Tesla. Given the surge in EV companies, it wouldn’t totally shock me if Tesla did vertically integrate and eventually revenue from battery sales overtook their revenue from car sales. Assuming that they took the dominant US market share. Somehow this turned into a Tesla bull thesis?

As I mentioned earlier, our dependence on China is proving to be quite the Achilles heel for the lithium-ion battery supply chain. There are several companies trying to prevent this, one of which has been backed by much maligned investor, Chamath Palihapitiya and his fund Social Capital. The company, Mitra Chem, manufactures “an iron-based cathode for application in non-Chinese batteries”. The ability to use iron was previously held under Chinese patent, which is set to expire soon. Once it does expire, Mitra Chem is free to produce and sell its iron-based battery chemistries freely. Now this is a Mitra Chem bull thesis.

I’m overdue for another full investment memo, but the close of this write-up will have to do for now. Mitra Chem is well positioned to solve the supply chain issue that EV manufacturers face when acquiring batteries. It’s also well suited to perform well given that batteries are both the most expensive part of the EV and the most critical to its performance. Tesla, GM, etc. will all be knocking on the Mitra Chem door. Per Chamath’s published investment thesis above, Mitra Chem also operates in the highest operating margin chemistry step of battery development. VCs often talk about why now and TAM when they evaluate investments. Both are pretty evident given everyday life and the proliferation of EVs everywhere. Investing in the company that manufactures a critical part of the most important and highest purchase-cost component for EVs feels like a great move.

EV battery production will play a similar role in future transportation economics to semiconductors today. While the scale may not be as large as something like semis, the market for high-quality, humane, and readily produceable/available batteries will be enormous as EVs expand past just cars. I see a world where a battery company can become the TSMC of the industry.