Ahead in the Clouds

Ahead in the Clouds

Commentary on the current market dip in software and why green grass lies ahead

When I changed careers from corporate cog to doing meaningful work at a startup, I realized quickly that the way that companies leverage technology is very different. While consulting is a personal example, that sentiment has been shared by plenty of colleagues who work in the corporate offices of other industries as well. I only experienced the switch from all things Office/Lotus Notes over to Google in 2016 or so. But that was just about it. Opportunities to use Tableau and Alteryx were dangled in front of us, but they were entirely project specific and required a more senior team member to submit an application, with request for fee approval. All things HR and internal ran through on-premise, branded software. Everything else more or less ran through Gmail, Powerpoint, and Excel.

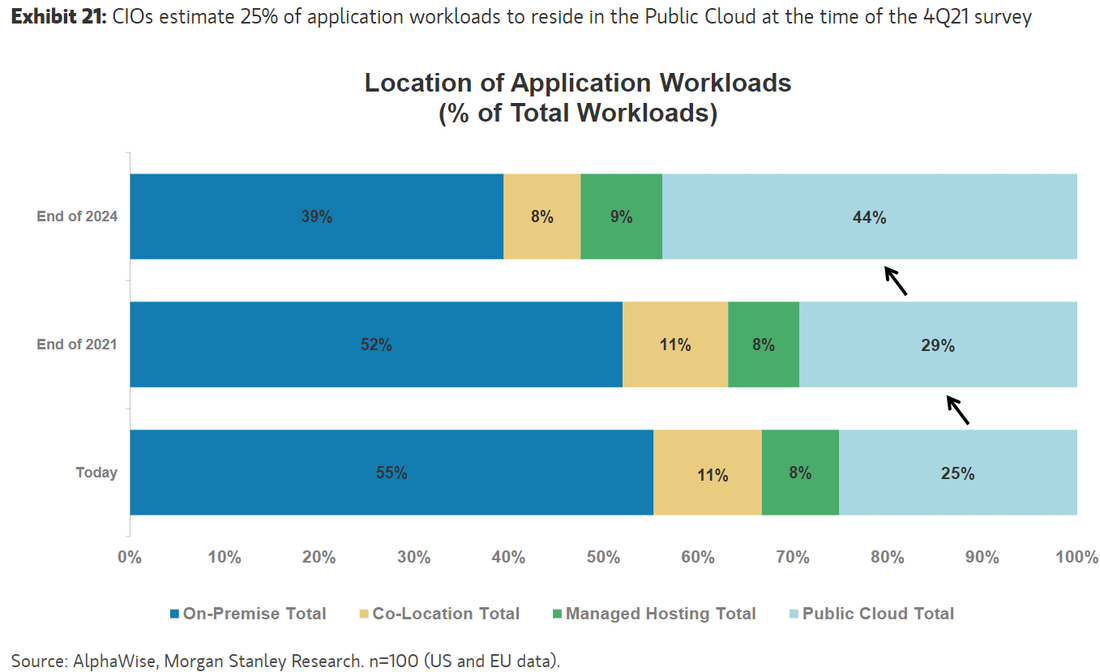

As evident in the quarterly Morgan Stanley CIO survey from Q4 2021, lack of technology adoption isn’t limited to just a handful of large companies. 55% of CIOs said that more than half of their company’s application workloads are handled via on-premise tools instead of the cloud.

This is a chart that’s looked similar-ish for the last five to ten years, but the light blue part has recently started to gain more momentum. While cliche, the line “it’s still the early innings for the cloud” is in my opinion more of a fact than a prediction. Per an extract from the excellent Clouded Judgement last week, CIOs for various large companies expect software spending to grow north of 5% in the next year, an increase compared to prior years.

One recent example of this is Ford’s recently signed five-year deal with Stripe. Stripe, your favorite company’s favorite company, is known for its payment processing software and APIs for anyone who sells anything over the internet. Ford’s Credit Co. CEO had the following to say:

Stripe’s platform will help us deliver simpler, outstanding payment experiences in any channel customers choose and scale improvements faster

Ford wants to improve the buyer and seller (in this case, dealer) experience and opted to partner with Stripe. Probably a wise choice. While I can’t say for certain, Ford falls into the camp of companies I would expect to opt for the “build” option when deciding between build or buy. Most Fortune 500 companies do. Signing a contract with Stripe, to me, is a bigger deal than most people will make it out to be. It’s indicative of a shift in mindset. Ford is one of the hundred biggest companies in the US and is not considered a technology company. Innovative, for sure, but not known for technology. It’s also one of the oldest companies in the top 100 by market cap. That’s a HUGE shift in mentality towards leveraging technology and the cloud.

Companies that don’t adapt to the changing landscape and speed with which business is done are going to lose. There’s a reason that tech stocks make up the heaviest weighting of the Fortune 500 and will continue to do so even after this blip. In this very adapt-or-die world we live in, where there is a constant threat of disruption for payments (Stripe, all of fintech), storage (Snowflake), tech infrastructure (Datadog, Cloudflare), the list goes on.

Tech companies have obviously benefitted greatly over the last year thanks to Covid and the push towards distributed companies. Cloud infrastructure has become more of a necessity than a luxury. Spending for engineering departments is critical both for legacy company growth and general operability. Neglecting areas mentioned above can result in hacks, faulty software, slow computing, and worse. As companies shift to becoming more developer centric and tech-enabled, CIOs/CTOs have more bargaining power. In Jamin’s newsletter I mentioned above, you’ll read that “0% of CIOs [expect IT] spend to decrease”.

The market is reacting differently, however. Cloud and tech stocks have taken a beatdown. The Nasdaq is down 10% this year. Valuations have been sliced in half or worse. A huge portion of the slide can be attributed to the Fed’s plans to raise interest rates. If you remember ZIRP, we’re seeing what happens when the opposite comes into play. As interest rates rise, money flows to the safe and secure yield as opposed to the risky, dollar generating assets out there. Compounding calls on the market are pushing everything lower in a snowball effect and many company multiples are at their pre-Covid levels. Multiples are how SaaS companies are valued, on a multiple of their revenue usually over twelve months (i.e. EV/NTM Revenue). Traders are pointing out stocks and indices trading below their 200-day moving average with calls for them to go lower.

Yet many of these beat down cloud and tech businesses are industry leaders for a reason. They have incredible gross margins, ARR growth, best in class net revenue retention, and solid CAC payback sustainability.

It feels like a lot of these stocks will continue to take hits and dip for parts of Q1, but it’s still a great buying opportunity in my opinion. I plan to dollar cost average my way into more of my bigger holdings right now. They’re trading at a discount yet still fundamentally are incredible businesses with ample room to grow. I’m also exploring other cloud companies (hi, $SNOW) which are approaching reasonably priced multiples. Slowly. We may not have hit a bottom yet, so proceed with caution. I’m still cash heavy, but there’s definitely an appealing opportunity presenting itself.